Release 0.9.5

v0.9.5Lots of new events to model real-life situations more closely

Webapp

Situation: Pillar 2 claim age and conversion rate

Pillar 2 settings now let you specify the core parameters of your pension fund, you can find them in your pension fund regulations and certificate:

- Earliest claim age. The legal default is 60, but some pension funds allow retirement from 58. This age is used when checking whether a Pillar 2 claim is allowed.

- Conversion rate. The all-inclusive conversion rate (umhüllender Umwandlungssatz / taux de conversion enveloppant) to convert your capital into a pension at age 65 if you draw a pension. You can override the default (currently 5.2%) with the value provided by your pension fund.

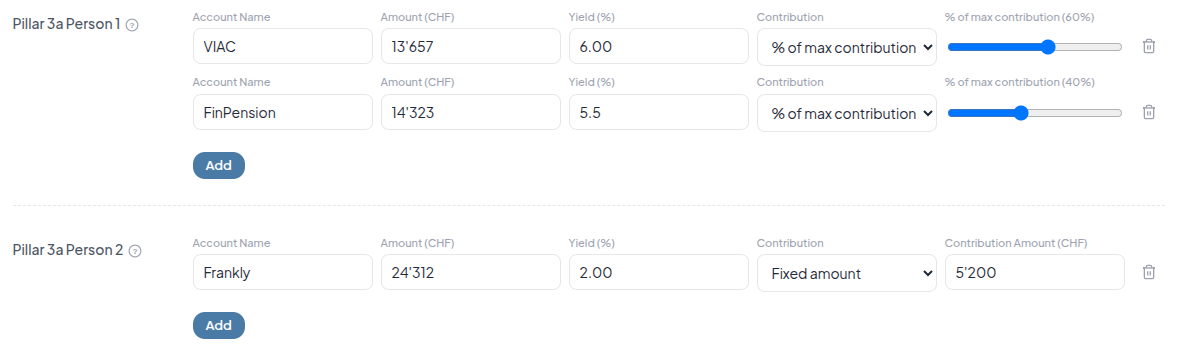

Situation: Pillar 3a and Pillar 3b contributions

Pillar 3a contributions can now be entered as either an amount or a percentage of the maximum (not just 100%). This makes it easier to split contributions across several Pillar 3a accounts (for example 60%/40%) — previously, setting “max” on more than one account would fail (issue 23).

Scenario: Relocate

A new event to change your residency location (where you pay your taxes) within Switzerland. (issue 193)

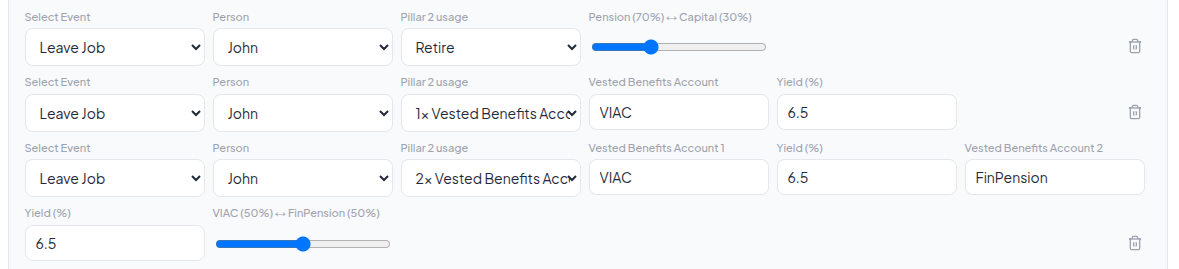

Scenario: Leave job

Retire from job and Quit job are now a single Leave job event. You choose what happens to your Pillar 2 money: retire with it, or move it to one or two vested accounts (issues 143, 159).

Scenario: Pillar 2 — pension or capital?

When you retire from a job, you can choose how much to take as a pension and how much as a lump sum (issue 52).

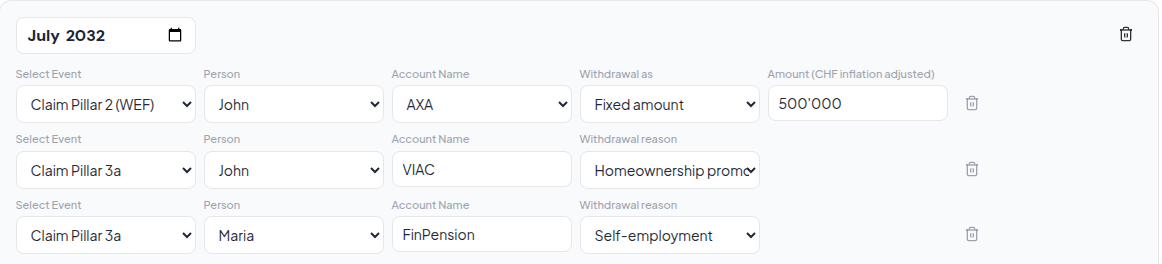

Scenario: Payout for WEF / self-employment

Pillar 2, vested account, and Pillar 3a payouts now include a reason. Payouts for self-employment or buying a primary home skip the usual age checks, but must respect the 3-year gap after a buy-in. For a home-purchase payout, the amount owed is tracked — it must be repaid before you can make further buy-ins (issue 184).

Scenario: Pillar 2 buy-in

New events for Pillar 2 buy-ins and for repaying earlier home-withdrawal payouts from Pillar 2 or vested accounts. Buy-ins are only allowed when no home-withdrawal payout is still outstanding. Repayments are not tax-deductible, but tax paid on the original withdrawal is refunded proportionally (issue 159).

Scenario: Leaving Switzerland

You can claim Pillar 2, vested accounts, and Pillar 3a/3b before age 60 if you are leaving Switzerland. All related accounts must be claimed in the same month. The capital moves to your cash account, minus retirement capital tax. The simulation then continues with Swiss taxes (your destination country is unknown to us), you are not charged the AHV contributions for non-gainfully employed person, which will lead to a contribution gap of a few years (issue 75).

Scenario: Repay mortgage

You can repay a mortgage with either a fixed amount or a percentage of the outstanding balance.

Scenario: Sell property

You can sell a home or rental property at its current value (adjusted for inflation) (issue 152).

Results: Scrollable table

Table column headers stay fixed while you scroll through the results (issue 195).

Results: Pillar 3a claims in the summary card

Pillar 3a claims now show correctly in the summary card for all account names, including multi-word names like “John Wayne”. The underlying claim always worked; only the display was wrong (issue 222).

Simulation Engine

Pillar 3a and Pillar 3b contributions

Contributions now use buy-in events instead of the legacy contribution asset, keeping behaviour consistent across the engine.

Pillar 2 and Vested Accounts, enforcement of delays

The simulation engine is now enforcing the relevant time constraints:

- no pillar 2 claim within 3 years of a buy-in

- no pillar 2 buy-ins if there is an outstanding pillar 2 property access claim (not paid back yet).